Bankruptcy Options for Florida Homeowners Facing Underwater Mortgages

Stop Foreclosure, Protect Your Home, and Get a Fresh Start – Chapter 7 vs Chapter 13 Explained

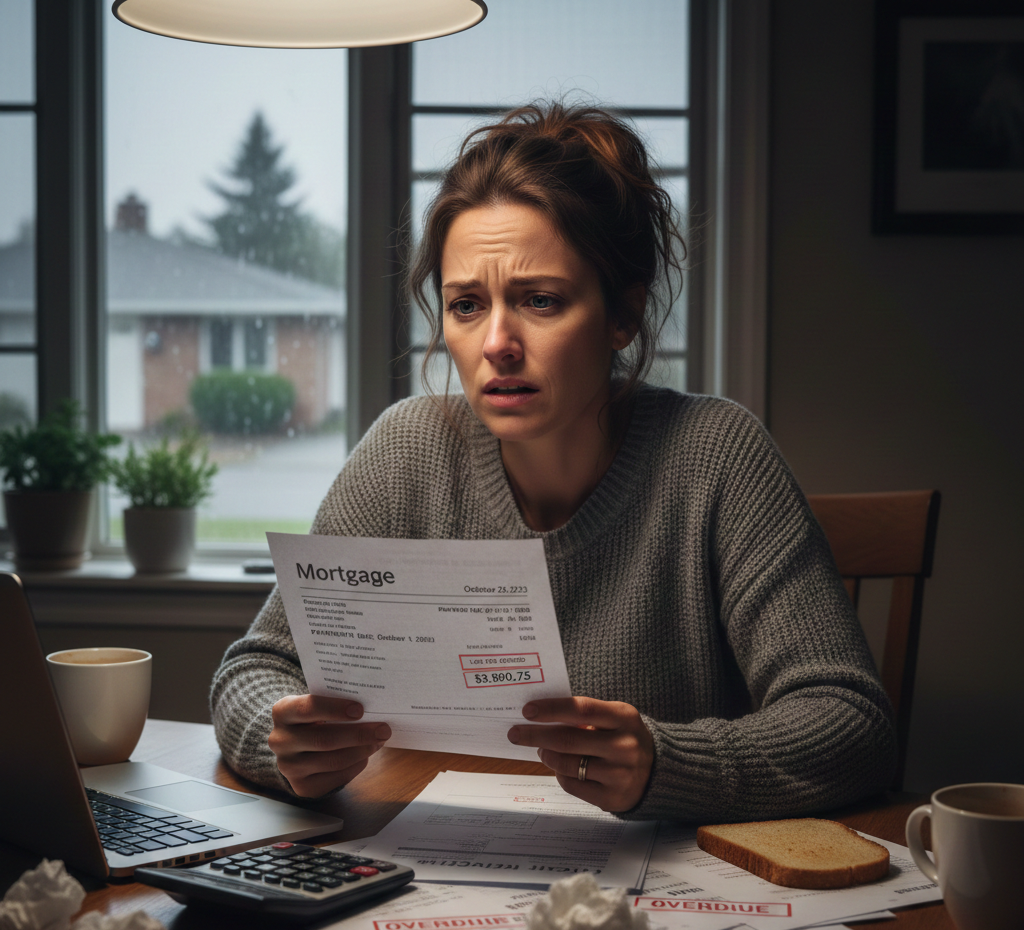

In Central Florida's shifting market, bankruptcy can be a powerful tool to halt foreclosure and restructure debt. We're here to guide you compassionately.

Download Your FREE Guide: Bankruptcy Options for Florida Homeowners

Instant Access: Chapter 7 vs 13 Comparison + Homestead Protection Tips

Or Call: 407-603-1664 | stacyann@realtorstephens.com

Important Legal Disclaimer: The information provided on this page is for general educational purposes only and does not constitute legal advice. Bankruptcy laws are complex and outcomes vary by individual circumstances. Realtor Stephens Team is not a law firm and cannot provide legal representation. We strongly recommend consulting a qualified Florida bankruptcy attorney to evaluate your specific situation and options. Do not rely on this content as a substitute for professional legal counsel.

Bankruptcy as a Tool for Central Florida Homeowners

As of December 2025, with home values softening in areas like Orlando and Kissimmee, many 2020-2023 buyers are underwater. Bankruptcy offers protections unavailable in short sales or deeds in lieu, including stopping foreclosure immediately via the automatic stay.

Realtor Stephens Team has helped families navigate these challenges – from short sales to referrals for bankruptcy support.

Chapter 7 vs Chapter 13 Bankruptcy: Side-by-Side for Florida Homeowners

| Aspect | Chapter 7 (Liquidation) | Chapter 13 (Repayment Plan) |

|---|---|---|

| Best For | Quick debt discharge; low income | Keeping home; catching up payments |

| Timeline | 3-6 months | 3-5 years |

| Home Impact | Stops foreclosure temporarily; often surrender | Stops foreclosure permanently; cure arrears |

| Lien Stripping | Not available | Yes – remove underwater junior liens |

| Homestead Protection | Unlimited if owned 1,215+ days | Same; plus repayment flexibility |

| Credit Report | 10 years | 7 years |

Florida Advantage: Unlimited homestead exemption protects all primary residence equity (with ownership requirements). Lien stripping in Chapter 13 can eliminate second mortgages if wholly unsecured.

Key Features for Florida Borrowers

- Automatic Stay: Immediately halts foreclosure sales and collections.

- Homestead Exemption: Protects unlimited equity in your primary home (up to ½ acre urban/160 acres rural) if owned 1,215+ days; otherwise ~$214,000 cap.

- Chapter 13 Lien Stripping: Strip junior liens if home value < first mortgage balance.

- Discharge: Wipe out unsecured debts; personal liability on mortgages.

Bankruptcy often complements real estate solutions like short sales. Consult professionals for your best path.

Explore Your Real Estate Options

407-603-1664 | stacyann@realtorstephens.com

Frequently Asked Questions: Bankruptcy for Florida Homeowners

What is the Florida homestead exemption in bankruptcy?

Unlimited equity protection for your primary residence if owned for at least 1,215 days; otherwise capped at approximately $214,000 (2025 federal limit).

Can Chapter 13 bankruptcy stop foreclosure in Florida?

Yes, the automatic stay halts foreclosure, and you can catch up arrears over 3-5 years while keeping your home.

What is lien stripping in Chapter 13?

Remove wholly underwater junior mortgages (e.g., second lien if home value < first mortgage balance), treating them as unsecured debt.

Chapter 7 vs Chapter 13: Which is better for keeping my home?

Chapter 13 is better for saving your home; Chapter 7 discharges debt faster but often leads to surrender if payments can't continue.

How can Realtor Stephens Team help?

We provide resources, referrals to attorneys, and guidance on real estate options like short sales alongside bankruptcy considerations.