Buy a Home in Florida Without Selling or Refinancing Your Out-of-State Home – Expert Strategies for 2026

Discover proven ways to secure your Florida dream home using bridge loans, HELOCs, and rental income – all while keeping your current property intact. Get your free personalized relocation guide today!

In 2026, Florida’s real estate market continues to attract out-of-state buyers with its no-income-tax advantage, booming economy, and median home prices around $400,000. But what if you’re ready to buy in Florida without selling or refinancing your current out-of-state home? This scenario is more common than you think, especially for snowbirds, relocators, or investors wanting to retain equity in their primary residence.

As leading Central Florida experts at Realtor Stephens Team, we’ve guided hundreds through this process. This comprehensive guide reveals the top strategies for “buying a home in Florida without selling current home,” including bridge loans, HELOCs, and leveraging rental income. We’ll cover Florida-specific mortgage requirements, pros/cons, and step-by-step advice to position you for success in a competitive market.

Ready to Buy in Florida Without Disruption?

Get expert guidance tailored to your situation. Download Your Free Relocation Guide Now! Or call 407-603-1664 today.

Top Strategies to Buy in Florida Without Selling or Refinancing Your Out-of-State Home

You don’t need to liquidate your current assets. Here are the most effective, lender-approved methods for 2026, focusing on Florida’s unique market.

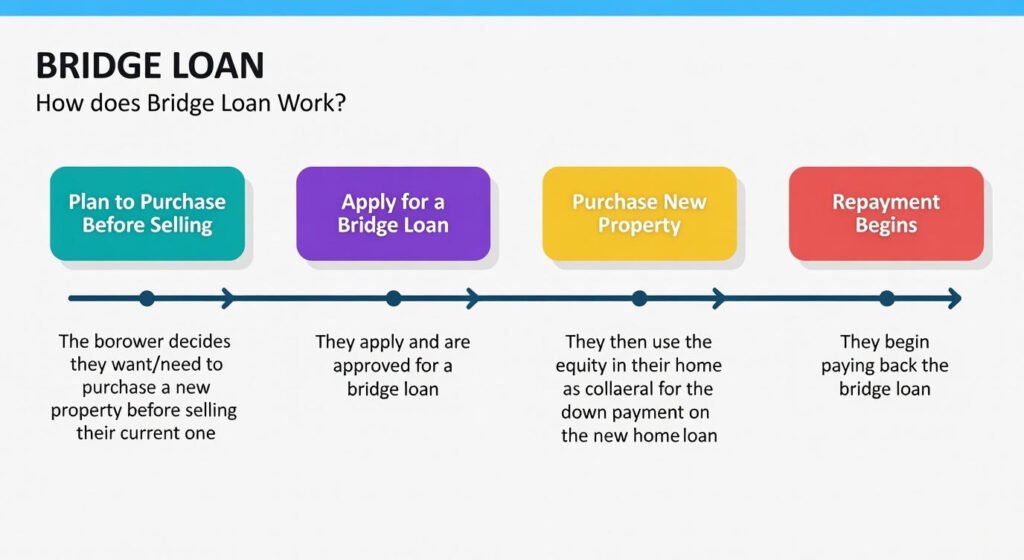

- Bridge Loans: The Fast-Track Option – A short-term loan (6-12 months) that uses your out-of-state home’s equity as collateral for a down payment on your Florida property. Rates hover at 8-12% in 2026, but no monthly payments until your old home sells. Florida lenders like Fidelity Home Group offer up to 80% LTV. Ideal if you expect a quick sale.

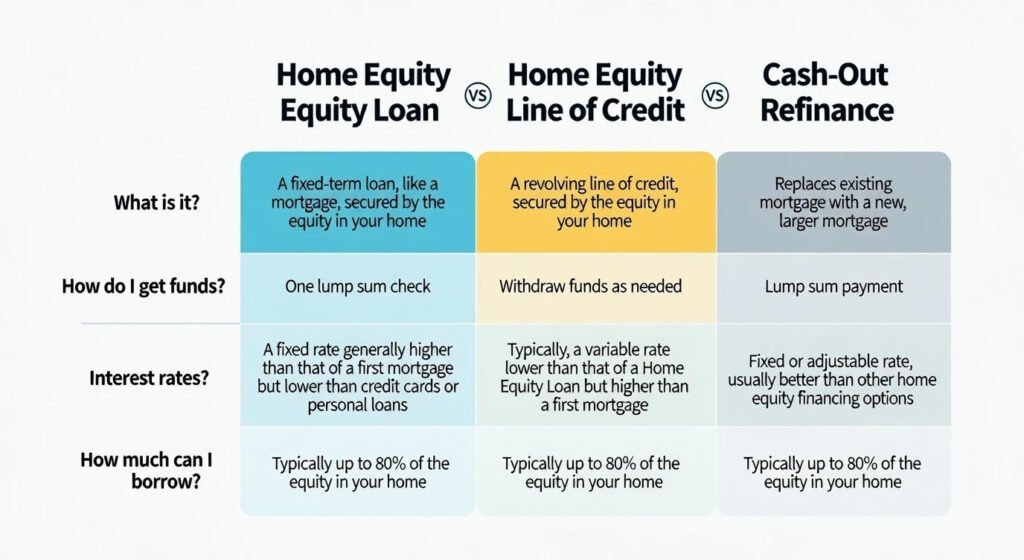

- HELOC (Home Equity Line of Credit): Flexible Equity Access – Borrow against your current home’s equity (up to 80-90% LTV) without refinancing. Use the line for a 10-20% down payment on your Florida home. Variable rates start at 8.5% in 2026; interest-only during draw period. Tax-deductible if used for home purchase. No need to sell – repay when convenient.

- Rent Out Your Current Home: Income-Qualifying Boost – Convert your out-of-state property to a rental and use 75% of the projected income to offset its mortgage, helping you qualify for a Florida loan. Need a signed lease and appraisal for fair market rent. In Florida’s investor-friendly market, this builds long-term wealth.

- Other Assets & Savings: Low-Risk Alternatives – Use 401(k) loans, gift funds, or liquid assets for down payments. Florida second-home buyers need 10%+ down; combine with strong DTI (<45%) and credit (640+).

Step-by-Step Process for Out-of-State Buyers in Florida

- Follow this roadmap to seamless success in Florida’s 2026 market, where inventory is balanced and remote closings are standard.

- Assess Your Finances: Get pre-approved for a second-home mortgage (DTI <45%, reserves 2-6 months). Calculate equity in your out-of-state home.

- Choose Your Strategy: Bridge for speed, HELOC for flexibility, or rental for income.

- Hire a Florida Realtor: Use virtual tours and remote expertise for neighborhoods like Orlando or Miami.

- Secure Financing: Apply for bridge/HELOC; provide lease if renting. Close Remotely: E-sign documents; inspect via video.

- Post-Purchase: Claim homestead exemption if primary; manage rental remotely

Don’t Risk Your Dream – Get Personalized Advice

Navigate Florida’s market with confidence. Request Your Free Guide Today!

Pros, Cons, and Florida-Specific Considerations

Pros: Retain low-rate mortgage, build wealth through rentals, no capital gains tax hit.

Cons: Higher interest on bridge/HELOC, dual property management. Florida perks: No income tax boosts affordability; homestead caps taxes for primaries.

FAQ: Buying in Florida Without Selling Your Out-of-State Home

Can I buy a home in Florida without selling my current out-of-state home?

Yes – use bridge loans, HELOCs, or rental income to qualify without liquidating your asset.

What are bridge loan requirements in Florida?

Up to 80% LTV, 6-12 month terms, rates 8-12%; repaid upon sale of old home.

How does renting my current home help qualify for a Florida mortgage?

Lenders use 75% of rental income to offset your old mortgage, improving DTI for the new loan.

What are second-home mortgage requirements in Florida?

640+ credit, DTI <45%, 10%+ down, 2-6 months reserves; no rental intent for classification.

Realtor Stephens Team | 407-603-1664 | stacyann@realtorstephens.com | www.realtorstephens.com

Central Florida Homes for Sale in Orlando Areas